1

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

__________________________

FORM

__________________________

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported):

__________________________

(Exact name of Registrant as Specified in Its Charter)

(State or Other Jurisdiction

of Incorporation)

(Commission File Number)

(IRS Employer

Identification No.)

,

,

(Address of Principal Executive Offices)

(Zip Code)

Registrant’s Telephone Number, Including Area Code: (

)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under

any of the following provisions:

☐

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

☐

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a -12)

☐

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

☐

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Trading

Symbol(s)

Name of each exchange on which registered

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933

(§ 230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§ 240.12b -2 of this chapter).

Emerging growth company

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for

complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

2

Item 2.02. Results of Operations and Financial Condition.

On April 23, 2026, USCB Financial Holdings, Inc. (the “Company”) issued a press release announcing its financial results for

the quarter ended March 31, 2026. A copy of the press release is furnished as Exhibit 99.1 to this Current Report on Form 8-K (“Form

8-K”) and is incorporated herein by reference.

The information in this Item 2.02, including Exhibit 99.1 hereto, is being furnished and shall not be deemed “filed” for purposes

of Section 18 of the Securities Exchange Act of 1934 (the “Exchange Act”), or otherwise be subject to the liability of that section, and

shall not be deemed to be incorporated by reference into any filing under the Securities Act of 1933 (the “Securities Act”) or the

Exchange Act except as expressly set forth by specific reference in such filing to this Form 8-K.

Item 7.01. Regulation FD Disclosure.

As previously announced, at 11:00 a.m. ET on April 24, 2026, the Company will hold an earnings conference call to discuss

its financial performance for the quarter ended March 31, 2026. A copy of the slides forming the basis of the presentation is being

furnished as Exhibit 99.2 to this Form 8-K and is incorporated herein by reference. A copy of the slides has also been posted to the

Company’s investor relations website, located at investors.uscenturybank.com.

The information in this Item 7.01, including Exhibit 99.2 hereto, is being furnished and shall not be deemed “filed” for purposes

of Section 18 of the Exchange Act, or otherwise be subject to the liability of that section, and shall not be deemed to be incorporated by

reference into any filing under the Securities Act or the Exchange Act except as set forth by specific reference in such filing to this Form

8-K.

Item 9.01. Financial Statements and Exhibits.

(d) Exhibits.

Exhibit No.

Description

99.1

99.2

104

Cover Page Interactive Data File (embedded within the Inline XBRL document)

3

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on

its behalf by the undersigned hereunto duly authorized.

USCB Financial Holdings, Inc.

By:

/s/ Robert Anderson

Name:

Robert Anderson

Title:

Chief Financial Officer

Date: April 23, 2026

1

Exhibit 99.1

EARNINGS RELEASE

USCB Financial Holdings, Inc. Delivers Record Quarter: $0.51 diluted EPS, up 33% over prior year. ROAA

1.34%, ROAE 17.07%, and 22% Year‑Over‑Year Net Income Growth.

MIAMI, FL – April 23, 2026 – USCB Financial Holdings, Inc. (the “Company”) (NASDAQ: USCB)

, the holding company for

U.S. Century Bank (the “Bank”), reported net income of $9.4 million or $0.51 per fully diluted share for the three months ended

March 31, 2026, compared with net income of $7.7 million or $0.38 per fully diluted share for the same period in 2025.

“The Company delivered a record quarter driven by strong core earnings performance and disciplined balance sheet execution. Diluted

earnings per share reached a record $0.51, while quarterly ROAA increased to 1.34%. Net income increased 22% year-over-year,

supported by 15.3% growth in net interest income, reflecting effective asset deployment and continued margin resilience. Credit quality

remained strong, underscoring the strength of the Company’s underwriting standards and risk management framework,” said Luis de la

Aguilera, Chairman, President, and CEO.

Unless otherwise stated, all percentage comparisons in the bullet points below are calculated at or for the quarter ended March 31, 2026

compared to at or for the quarter ended March 31, 2025 and annualized where appropriate.

Profitability

•

Annualized return on average assets for the quarter ended March 31, 2026 was 1.34% compared to 1.19% for the first quarter of

2025.

•

Annualized return on average stockholders’ equity for the quarter ended March 31, 2026 was 17.07% compared to 14.15% for the

first quarter of 2025.

•

The efficiency ratio for the quarter ended March 31, 2026 was 52.34% compared to 52.79% for the first quarter of 2025.

•

Net interest margin for the quarter ended March 31, 2026 was 3.27 % compared to 3.10% for the first quarter of 2025.

•

Net interest income before provision for credit losses was $22.0 million for the quarter ended March 31, 2026, an increase of $2.9

million or 15.3% compared to $19.1 million for the same period in 2025.

•

The Company recognized a $619 thousand income tax benefit in the first quarter of 2026 due to an adjustment to the deferred tax

asset calculation from 2025.

Balance Sheet

•

Total assets were $2.8 billion at March 31, 2026, representing an increase of $168.4 million or 6.3% from $2.7 billion at March 31,

2025.

•

Total loans held for investment were $2.2 billion at March 31, 2026, representing an increase of $204.8 million or 10.1% from $2.0

billion at March 31, 2025.

•

Total deposits were $2.5 billion at March 31, 2026, representing an increase of $184.0 million or 8.0% from $2.3 billion at

March 31, 2025.

•

Total stockholders’ equity was $223.2 million at March 31, 2026, representing a decrease of $1.8 million or 0.8% from $225.1

million at March 31, 2025. Total stockholders’ equity included accumulated other comprehensive loss of $31.3 million at March 31,

2026 compared to accumulated other comprehensive loss of $41.1 million at March 31, 2025. The decrease in total stockholders’

equity was driven primarily by the repurchase of 2.0 million shares of Class A common stock conducted in September 2025 as

previously disclosed.

2

Asset Quality

•

The allowance for credit losses (“ACL”) increased by $1.4 million to $26.1 million at March 31, 2026 from $24.7 million at

March 31, 2025.

•

The ACL represented 1.16% of total loans at March 31, 2026 and 1.22% of total loans at March 31, 2025.

•

The provision for credit loss was $801 thousand for the quarter ended March 31, 2026, an increase of $120 thousand compared to

$681 thousand for the same period in 2025.

•

The ratio of non-performing loans to total loans was 0.16% for the quarter ended March 31, 2026 and 0.20% for the quarter ended

March 31, 2025. Non-performing loans totaled $3.6 million at March 31, 2026 and $4.2 million at March 31, 2025.

Non-interest Income and Non-interest Expense

•

Non-interest income was $4.2 million for the three months ended March 31, 2026, an increase of $434 thousand or 11.7% compared

to $3.7 million for the same period in 2025.

•

Non-interest expense was $13.7 million for the three months ended March 31, 2026, an increase of $1.7 million or 13.8% compared

to $12.1 million for the three months ended March 31, 2025.

Capital

•

On April 20, 2026, the Company’s Board of Directors declared a quarterly cash dividend of $0.125 per share of the Company’s

Class A common stock. The dividend will be paid on June 5, 2026 to shareholders of record at the close of business on May 15,

2026.

•

As of March 31, 2026,

total risk-based capital ratios for the Company and the Bank were 14.09% and 13.96%, respectively, well in

excess of regulatory requirements (only applicable to the Bank currently) .

•

Tangible book value per common share (non-GAAP financial measure) was $12.23 at March 31, 2026, representing an increase of

$1.00 or 8.9% from $11.23 at March 31, 2025. At March 31, 2026, tangible book value per common share was negatively affected

by ($1.72) per share due to an accumulated other comprehensive loss of $31.3 million mostly due to changes in the market value

of the Company’s available for sale securities. At March 31, 2025, tangible book value per common share was negatively affected

by ($2.05) per share due to an accumulated other comprehensive loss of $41.1 million.

Conference Call and Webcast

The Company will host a conference call on Friday, April 24, 2026, at 11:00 a.m. Eastern Time to discuss the Company’s unaudited

financial results for the quarter ended March 31, 2026. To access the conference call, dial (833) 816-1416 (U.S. toll-free) and ask to join

the USCB Financial Holdings Call.

Additionally, interested parties can listen to a live webcast of the call in the “Investor Relations” section of the Company’s website

at www.uscentury.com . An archived version of the webcast will be available in the same location shortly after the live call has ended.

About USCB Financial Holdings, Inc.

USCB Financial Holdings, Inc. is the bank holding company for U.S. Century Bank. Established in 2002, U.S. Century Bank is one of

the largest community banks headquartered in Miami, and one of the largest community banks in the State of Florida. U.S. Century

Bank is rated 5-Stars by BauerFinancial, the nation’s leading independent bank rating firm. U.S. Century Bank offers customers a wide

range of financial products and services and supports numerous community organizations, including the Greater Miami Chamber of

Commerce, the South Florida Hispanic Chamber of Commerce, and ChamberSouth. For more information about us or to find a banking

center near you, please call (305) 715-5200 or visit www.uscentury.com.

Forward-Looking Statements

This earnings release may contain statements that are not historical in nature and are intended to be, and are hereby identified as, forward-

looking statements for purposes of the safe harbor provided by Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements are those that are not historical facts. The words “may,” “will,” “anticipate,” “could,” “should,” “would,”

“believe,” “contemplate,” “expect,” “aim,” “plan,” “estimate,” “seek,” “continue,” and “intend,”, the negative of these terms, as well as

other similar words and expressions of the future, are intended to identify forward-looking statements. These forward-looking statements

include, but are not limited to, statements related to our projected growth, anticipated future financial performance, and management’s

3

long-term performance goals, as well as statements relating to the anticipated effects on our results of operations and financial condition

from expected or potential developments or events, or business and growth strategies, including anticipated internal growth and potential

future additional balance sheet restructuring.

These forward-looking statements involve significant risks and uncertainties that could cause our actual results to differ materially from

those anticipated in such statements. Potential risks and uncertainties include, but are not limited to:

•

the strength of the United States economy in general and the strength of the local economies in which we conduct operations;

•

our ability to successfully manage interest rate risk, credit risk, liquidity risk, and other risks inherent to our industry;

•

the accuracy of our financial statement estimates and assumptions, including the estimates used for our allowance for credit losses

and deferred tax asset valuation allowance;

•

the efficiency and effectiveness of our internal control procedures and processes;

•

our ability to comply with the extensive laws and regulations to which we are subject, including the laws for each jurisdiction where

we operate;

•

adverse changes or conditions in capital and financial markets, including actual or potential stresses in the banking industry;

•

deposit attrition and the level of our uninsured deposits;

•

legislative or regulatory changes, including the enactment of the One Big Beautiful Bill and changes in accounting principles,

policies, practices or guidelines, including the on-going effects of the Current Expected Credit Losses (“CECL”) standard;

•

the lack of a significantly diversified loan portfolio and our concentration in the South Florida market, including the risks of

geographic, depositor, and industry concentrations, including our concentration in loans secured by real estate, in particular,

commercial real estate;

•

the effects of climate change;

•

the concentration of ownership of our common stock;

•

fluctuations in the price of our common stock;

•

our ability to fund or access the capital markets at attractive rates and terms and manage our growth, both organic growth as well

as growth through other means, such as future acquisitions;

•

inflation, interest rate, unemployment rate, and market and monetary fluctuations;

•

the effects of potential new or increased tariffs, retaliatory tariffs and trade restrictions;

•

the impact of international hostilities and geopolitical events;

•

increased competition and its effect on the pricing of our products and services as well as our interest rate spread and net interest

margin;

•

the loss of key employees;

•

the effectiveness of our risk management strategies, including operational risks, including, but not limited to, client, employee, or

third-party fraud and security breaches; and

•

other risks described in this earnings release and other filings we make with the Securities and Exchange Commission (“SEC”).

All forward-looking statements are necessarily only estimates of future results, and there can be no assurance that actual results will

not differ materially from expectations. Therefore, you are cautioned not to place undue reliance on any forward-looking statements.

Further, forward-looking statements included in this earnings release are made only as of the date hereof, and we undertake no obligation

to update or revise any forward-looking statement to reflect events or circumstances after the date on which the statements are made or

to reflect the occurrence of unanticipated events, unless required to do so under the federal securities laws. You should also review the

risk factors described in the reports the Company has filed or will file with the SEC.

Non-GAAP Financial Measures

This earnings release includes financial information determined by methods other than in accordance with generally accepted accounting

principles (“GAAP”). This financial information includes certain operating performance measures. Management has included these non-

GAAP measures because it believes these measures may provide useful supplemental information for evaluating the Company’s

operations and underlying performance trends. Further, management uses these measures in managing and evaluating the Company’s

business and intends to refer to them in discussions about our operations and performance. Operating performance measures should be

viewed in addition to, and not as an alternative to or substitute for, measures determined in accordance with GAAP, and are not

necessarily comparable to non-GAAP measures that may be presented by other companies. Reconciliations of these non-GAAP

measures to the most directly comparable GAAP measures can be found in the ‘Non-GAAP Reconciliation Tables’ included in the

exhibits to this earnings release.

All numbers included in this press release are unaudited unless otherwise noted.

4

Contacts:

Investor Relations

InvestorRelations@uscentury.com

Media Relations

Martha Guerra-Kattou

MGuerra@uscentury.com

5

USCB FINANCIAL HOLDINGS, INC.

CONSOLIDATED STATEMENTS OF INCOME (UNAUDITED)

(Dollars in thousands, except per share data)

Three Months Ended March 31,

2026

2025

Interest income:

Loans, including fees

$

32,789

$

30,245

Investment securities

3,411

3,024

Interest-bearing deposits in financial institutions

832

709

Total interest income

37,032

33,978

Interest expense:

Interest-bearing checking deposits

310

338

Savings and money market deposits

8,133

9,335

Time deposits

4,700

3,918

FHLB advances

1,040

1,272

Subordinated notes

801

-

Total interest expense

14,984

14,863

Net interest income before provision for credit losses

22,048

19,115

Provision for credit losses

801

681

Net interest income after provision for credit losses

21,247

18,434

Non-interest income:

Service fees

3,100

2,331

Gain on sale of securities available for sale, net

14

-

Gain on sale of loans held for sale, net

106

525

Other non-interest income

930

860

Total non-interest income

4,150

3,716

Non-interest expense:

Salaries and employee benefits

8,570

7,636

Occupancy

1,316

1,284

Regulatory assessments and fees

484

421

Consulting and legal fees

561

193

Network and information technology services

560

505

Other operating expense

2,220

2,013

Total non-interest expense

13,711

12,052

Income before income tax expense

11,686

10,098

Income tax expense

2,335

2,440

Net income

$

9,351

$

7,658

Per share information:

Net income per common share, basic

$

0.51

$

0.38

Net income per common share, diluted

$

0.51

$

0.38

Cash dividends declared

$

0.125

$

0.10

Weighted average shares outstanding:

Common shares, basic

18,214,041

20,020,933

Common shares, diluted

18,454,006

20,319,535

6

USCB FINANCIAL HOLDINGS, INC.

SELECTED FINANCIAL DATA (UNAUDITED)

(Dollars in thousands, except per share data)

As of or For the Three Months Ended

3/31/2026

12/31/2025

9/30/2025

6/30/2025

3/31/2025

Income statement data:

Net interest income before provision for credit losses

$

22,048

$

22,207

$

21,274

$

21,034

$

19,115

Provision for credit losses

801

480

105

1,031

681

Net interest income after provision for credit losses

21,247

21,727

21,169

20,003

18,434

Service fees

3,100

2,209

2,661

2,402

2,331

Gain (loss) on sale of securities available for sale, net

14

(7,498)

(28)

-

-

Gain on sale of loans held for sale, net

106

197

128

151

525

Other non-interest income

930

914

923

817

860

Total non-interest income

4,150

(4,178)

3,684

3,370

3,716

Salaries and employee benefits

8,570

8,668

7,909

7,954

7,636

Occupancy

1,316

1,327

1,382

1,337

1,284

Regulatory assessments and fees

484

443

377

396

421

Consulting and legal fees

561

900

585

263

193

Network and information technology services

560

599

656

564

505

Other operating expense

2,220

2,338

2,139

2,120

2,013

Total non-interest expense

13,711

14,275

13,048

12,634

12,052

Net income before income tax expense

11,686

3,274

11,805

10,739

10,098

Income tax expense

2,335

1,911

2,866

2,599

2,440

Net income

$

9,351

$

1,363

$

8,939

$

8,140

$

7,658

Per share information:

Net income per common share, basic

$

0.51

$

0.08

$

0.46

$

0.41

$

0.38

Net income per common share, diluted

$

0.51

$

0.07

$

0.45

$

0.40

$

0.38

Cash dividends declared

$

0.125

$

0.10

$

0.10

$

0.10

$

0.10

Balance sheet data (at period-end):

Cash and cash equivalents

$

78,963

$

38,477

$

56,811

$

54,819

$

97,984

Securities available-for-sale

$

277,160

$

307,490

$

324,179

$

285,382

$

275,139

Securities held-to-maturity

$

149,931

$

153,941

$

156,365

$

158,740

$

161,790

Total securities

$

427,091

$

461,431

$

480,544

$

444,122

$

436,929

Loans held for investment

(1)

$

2,241,051

$

2,189,257

$

2,130,966

$

2,113,318

$

2,036,212

Allowance for credit losses

$

(26,102)

$

(25,500)

$

(24,964)

$

(24,933)

$

(24,740)

Total assets

$

2,845,735

$

2,791,540

$

2,767,945

$

2,719,474

$

2,677,382

Non-interest-bearing demand deposits

$

620,714

$

583,860

$

584,240

$

584,895

$

605,489

Interest-bearing deposits

$

1,872,866

$

1,761,220

$

1,871,374

$

1,750,766

$

1,704,080

Total deposits

$

2,493,580

$

2,345,080

$

2,455,614

$

2,335,661

$

2,309,569

FHLB advances

$

53,000

$

158,250

$

11,000

$

108,000

$

108,000

Subordinated notes

$

39,338

$

39,300

$

39,262

$

-

$

-

Total liabilities

$

2,622,489

$

2,574,357

$

2,558,850

$

2,487,891

$

2,452,294

Total stockholders' equity

$

223,246

$

217,183

$

209,095

$

231,583

$

225,088

Capital ratios:

(2)

Leverage ratio

8.61%

8.46%

8.47%

9.72%

9.61%

Common equity tier 1 capital

11.09%

10.92%

11.17%

12.52%

12.48%

Tier 1 risk-based capital

11.09%

10.92%

11.17%

12.52%

12.48%

Total risk-based capital

14.09%

13.91%

14.20%

13.73%

13.72%

(1) Loan amounts include deferred fees/costs.

(2) Reflects the Company's regulatory capital ratios which are provided for informational purposes only; as a small bank holding company, the Company is not subject

to regulatory capital requirements. The Bank's total risk-based capital at March 31, 2026 was 13.96%.

7

USCB FINANCIAL HOLDINGS, INC.

AVERAGE BALANCES, RATIOS, AND OTHER DATA (UNAUDITED)

(Dollars in thousands)

As of or For the Three Months Ended

3/31/2026

12/31/2025

9/30/2025

6/30/2025

3/31/2025

Average balance sheet data:

Cash and cash equivalents

$

112,107

$

82,338

$

139,389

$

71,388

$

82,610

Securities available-for-sale

$

295,065

$

332,356

$

299,892

$

281,840

$

265,154

Securities held-to-maturity

$

152,144

$

155,269

$

157,702

$

160,443

$

163,510

Total securities

$

447,209

$

487,625

$

457,594

$

442,283

$

428,664

Loans held for investment

(1)

$

2,177,734

$

2,130,898

$

2,099,043

$

2,057,445

$

1,986,856

Total assets

$

2,834,717

$

2,799,863

$

2,798,115

$

2,677,198

$

2,606,593

Interest-bearing deposits

$

1,842,283

$

1,857,218

$

1,887,545

$

1,710,568

$

1,652,147

Non-interest-bearing demand deposits

$

584,784

$

595,969

$

569,522

$

580,121

$

563,040

Total deposits

$

2,427,067

$

2,453,187

$

2,457,067

$

2,290,689

$

2,215,187

FHLB advances

$

110,045

$

51,462

$

40,065

$

116,527

$

138,944

Subordinated notes

$

39,313

$

39,287

$

26,029

$

-

$

-

Total liabilities

$

2,612,491

$

2,587,470

$

2,572,799

$

2,448,706

$

2,387,088

Total stockholders' equity

$

222,226

$

212,393

$

225,316

$

228,492

$

219,505

Performance ratios:

Return on average assets

(2)

1.34%

0.19%

1.27%

1.22%

1.19%

Return on average equity

(2)

17.07%

2.55%

15.74%

14.29%

14.15%

Net interest margin

(2)

3.27%

3.27%

3.14%

3.28%

3.10%

Non-interest income to average assets

(2)

0.59%

(0.59)%

0.52%

0.50%

0.58%

Non-interest expense to average assets

(2)

1.96%

2.02%

1.85%

1.89%

1.88%

Efficiency ratio

(3)

52.34%

79.18%

52.28%

51.77%

52.79%

Loans by type (at period end):

(4)

Residential real estate

$

346,917

$

307,692

$

316,557

$

307,020

$

301,164

Commercial real estate

$

1,259,642

$

1,244,835

$

1,226,121

$

1,206,621

$

1,150,129

Commercial and industrial

$

291,333

$

295,548

$

269,430

$

263,966

$

256,326

Correspondent banks

$

128,722

$

127,968

$

104,598

$

110,155

$

103,026

Consumer and other

$

207,794

$

207,215

$

207,939

$

218,426

$

218,711

Asset quality data:

Allowance for credit losses to total loans

1.16%

1.16%

1.17%

1.18%

1.22%

Allowance for credit losses to non-performing loans

717%

813%

1906%

1825%

595%

Total non-performing loans

(5)

$

3,640

$

3,138

$

1,310

$

1,366

$

4,156

Non-performing loans to total loans

0.16%

0.14%

0.06%

0.06%

0.20%

Non-performing assets to total assets

(5)

0.13%

0.11%

0.05%

0.05%

0.16%

Net charge-offs (recoveries of) to average loans

(2)

(0.00)%

(0.00)%

(0.00)%

0.14%

0.00%

Net charge-offs (recovery) of credit losses

$

(4)

$

(11)

$

(4)

$

702

$

2

Interest rates and yields:

(2)

Loans held for investment

6.11%

6.16%

6.21%

6.23%

6.17%

Investment securities

3.05%

3.01%

3.03%

3.06%

2.81%

Total interest-earning assets

5.49%

5.54%

5.56%

5.64%

5.51%

Deposits

(6)

2.20%

2.28%

2.53%

2.46%

2.49%

FHLB advances

3.83%

3.91%

3.73%

3.72%

3.71%

Subordinated notes

8.26%

8.09%

6.16%

-

-

Total interest-bearing liabilities

3.05%

3.14%

3.34%

3.32%

3.37%

Other information:

Full-time equivalent employees

211

204

206

203

201

(1) Loan amounts include deferred fees/costs.

(2) Annualized.

(3) Efficiency ratio is defined as total non-interest expense divided by sum of net interest income and total non-interest income.

(4) Loan amounts exclude deferred fees/costs.

(5) The amounts for total non-performing loans and total non-performing assets are the same at the dates presented since there was no other real estate owned (OREO)

recorded at any of the dates presented.

(6) Reflects effect of non-interest-bearing deposits.

8

USCB FINANCIAL HOLDINGS, INC.

NET INTEREST MARGIN (UNAUDITED)

(Dollars in thousands)

Three Months Ended March 31,

2026

2025

Average

Balance

Interest

Yield/Rate

(1)

Average

Balance

Interest

Yield/Rate

(1)

Assets

Interest-earning assets:

Loans held for investment

(2)

$

2,177,734

$

32,789

6.11%

$

1,986,856

$

30,245

6.17%

Investment securities

(3)

454,262

3,411

3.05%

436,935

3,024

2.81%

Other interest-earning assets

105,457

832

3.20%

75,182

709

3.82%

Total interest-earning assets

2,737,453

37,032

5.49%

2,498,973

33,978

5.51%

Non-interest-earning assets

97,264

107,620

Total assets

$

2,834,717

$

2,606,593

Liabilities and stockholders' equity

Interest-bearing liabilities:

Interest-bearing checking deposits

$

52,099

310

2.41%

$

53,611

338

2.56%

Saving and money market deposits

1,256,418

8,133

2.63%

1,199,027

9,335

3.16%

Time deposits

533,766

4,700

3.57%

399,509

3,918

3.98%

Total interest-bearing deposits

1,842,283

13,143

2.89%

1,652,147

13,591

3.34%

FHLB advances

110,045

1,040

3.83%

138,944

1,272

3.71%

Subordinated notes

39,313

801

8.26%

-

-

- %

Total interest-bearing liabilities

1,991,641

14,984

3.05%

1,791,091

14,863

3.37%

Non-interest-bearing demand deposits

584,784

563,040

Other non-interest-bearing liabilities

36,066

32,957

Total liabilities

2,612,491

2,387,088

Stockholders' equity

222,226

219,505

Total liabilities and stockholders' equity

$

2,834,717

$

2,606,593

Net interest income

$

22,048

$

19,115

Net interest spread

(4)

2.44%

2.14%

Net interest margin

(5)

3.27%

3.10%

(1) Annualized.

(2) Average loan balances include non-accrual loans. Interest income on loans includes accretion of deferred loan fees, net of deferred loan costs.

(3) At fair value except for securities held to maturity. This amount includes FHLB stock.

(4) Net interest spread is the average yield earned on total interest-earning assets minus the average rate paid on total interest-bearing liabilities.

(5) Net interest margin is the ratio of net interest income to total interest-earning assets.

9

USCB FINANCIAL HOLDINGS, INC.

NON-GAAP FINANCIAL MEASURES (UNAUDITED)

(Dollars in thousands)

As of or For the Three Months Ended

3/31/2026

12/31/2025

9/30/2025

6/30/2025

3/31/2025

Pre-tax pre-provision ("PTPP") income:

(1)

Net income

$

9,351

$

1,363

$

8,939

$

8,140

$

7,658

Plus: Income tax expense

2,335

1,911

2,866

2,599

2,440

Plus: Provision for credit losses

801

480

105

1,031

681

PTPP income

$

12,487

$

3,754

$

11,910

$

11,770

$

10,779

PTPP return on average assets:

(1)

PTPP income

$

12,487

$

3,754

$

11,910

$

11,770

$

10,779

Average assets

$

2,834,717

$

2,799,863

$

2,798,115

$

2,677,198

$

2,606,593

PTPP return on average assets

(2)

1.79%

0.53%

1.69%

1.76%

1.68%

Operating net income:

(1)

Net income

$

9,351

$

1,363

$

8,939

$

8,140

$

7,658

Less: Net gains (losses) on sale of securities

14

(7,498)

(28)

-

-

Less: Tax effect on sale of securities

(4)

1,900

7

-

-

Plus: Tax (benefit) liability expense from prior periods

(619)

(3)

1,096

(4)

-

-

-

Operating net income

$

8,722

$

8,057

$

8,960

$

8,140

$

7,658

Operating return on average assets:

(1)

Operating net income

$

8,722

$

8,057

$

8,960

$

8,140

$

7,658

Average assets

$

2,834,717

$

2,799,863

$

2,798,115

$

2,677,198

$

2,606,593

Operating net income return on average assets

(2)

1.25%

1.14%

1.27%

1.22%

1.19%

Operating return on average equity:

(1)

Operating net income

$

8,722

$

8,057

$

8,960

$

8,140

$

7,658

Average equity

$

222,226

$

212,393

$

225,316

$

228,492

$

219,505

Operating net income return on average equity

(2)

15.92%

15.05%

15.78%

14.29%

14.15%

Operating revenue:

(1)

$

22,048

$

22,207

$

21,274

$

21,034

$

19,115

4,150

(4,178)

3,684

3,370

3,716

14

(7,498)

(28)

-

-

$

26,184

$

25,527

$

24,986

$

24,404

$

22,831

Operating efficiency ratio:

(1)

$

13,711

$

14,275

$

13,048

$

12,634

$

12,052

$

26,184

$

25,527

$

24,986

$

24,404

$

22,831

52.36%

55.92%

52.22%

51.77%

52.79%

(1) The Company believes these non-GAAP financial measurements are key indicators of the ongoing earnings power of the Company.

(2) Annualized.

(3) The Company recognized a $619 thousand income tax benefit in first quarter of 2026 due to an adjustment to the deferred tax asset calculation from 2025.

(4) State tax liability expenses for 2024 and for the first three quarters of 2025 were recognized during the fourth quarter of 2025. The state tax expense is related to

taxes due on interest income on loans whose collateral are located outside of the State of Florida.

10

USCB FINANCIAL HOLDINGS, INC.

NON-GAAP FINANCIAL MEASURES (UNAUDITED)

(Dollars in thousands, except per share data)

As of or For the Three Months Ended

3/31/2026

12/31/2025

9/30/2025

6/30/2025

3/31/2025

Tangible book value per common share (at period-end):

(1)(4)

Total stockholders' equity

$

223,246

$

217,183

$

209,095

$

231,583

$

225,088

Less: Intangible assets

-

-

-

-

-

Tangible stockholders' equity

$

223,246

$

217,183

$

209,095

$

231,583

$

225,088

Total shares issued and outstanding (at period-end):

Total common shares issued and outstanding

18,257,400

18,137,885

18,107,385

20,078,385

20,048,385

Tangible book value per common share

(2)

$

12.23

$

11.97

$

11.55

$

11.53

$

11.23

Operating diluted net income per common share:

(1)

Operating net income

$

8,722

$

8,057

$

8,960

$

8,140

$

7,658

Total weighted average diluted shares of common stock

18,454,006

18,348,725

19,755,820

20,295,794

20,319,535

Operating diluted net income per common share:

$

0.47

$

0.44

0.45

0.40

0.38

Tangible Common Equity/Tangible Assets

(1)(4)

$

223,246

$

217,183

$

209,095

$

231,583

$

225,088

(3)

$

2,845,735

2,791,540

2,767,945

2,719,474

2,677,382

Tangible Common Equity/Tangible Assets

7.84%

7.78%

7.55%

8.52%

8.41%

(1) The Company believes these non-GAAP financial measurements are key indicators of the ongoing earnings power of the Company.

(2) Excludes the dilutive effect, if any, of shares of common stock issuable upon exercise of outstanding stock options.

(3) Since the Company has no intangible assets, tangible stockholders’ equity and tangible total assets are the same amounts as stockholders’ equity and total assets,

respectively, as calculated under GAAP.

(4) The decrease in total stockholders’ equity was driven primarily by the repurchase of 2.0 million shares of Class A common stock conducted in September 2025.

Exhibit 99.2

USCB FINANCIAL HOLDINGS EARNINGS PRESENTATION FIRST QUARTER 2026 NASDAQ: USCB

FORWARD-LOOKING STATEMENTS This presentation may contain statements that are not historical in nature and are intended to be, and are hereby identified as, forward-looking statements for purposes of the safe harbor provided by Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are those that are not historical facts. The words “may,” “will,” “anticipate,” “could,” “ should,” “would,” “believe,” “contemplate,” “expect,” “aim,” “plan,” “estimate,” “continue,” “seek,” and “intend,” the negative of these terms, as well as other similar words and expressions of the future, are intended to identify forward-looking statements. These forward-looking statements include, but are not limited to, statements related to our projected growth, anticipated future financial performance, and management’s long-term performance goals, as well as statements relating to the anticipated effects on our results of operations and financial condition from expected or potential developments or events, or business and growth strategies, including anticipated internal growth and potential future additional balance sheet restructuring. All numbers included in this presentation are unaudited unless otherwise noted. These forward-looking statements involve significant risks and uncertainties that could cause our actual results to differ materially from those anticipated in such statements. Potential risks and uncertainties include, but are not limited to: the strength of the United States economy in general and the strength of the local economies in which we conduct operations; our ability to successfully manage interest rate risk, credit risk, liquidity risk, and other risks inherent to our industry; the accuracy of our financial statement estimates and assumptions, including the estimates used for our allowance for credit losses and deferred tax asset valuation allowance; the efficiency and effectiveness

of our internal control procedures and processes; our ability to comply with the extensive laws and regulations to which we are subject, including the laws for each jurisdiction where we operate; adverse changes or conditions in the capital and financial markets, including actual or potential stresses in the banking industry; deposit attrition and the level of our uninsured deposits; legislative or regulatory changes and changes, including the enactment of the One Big Beautiful Bill, in accounting principles, policies, practices or guidelines, including the on-going effects of the implementation of the Current Expected Credit Losses (“CECL”) standard; the lack of a significantly diversified loan portfolio and our concentration in the South Florida market, including the risks of geographic, depositor, and industry concentrations, including our concentration in loans secured by real estate, in particular, commercial real estate; the effects of climate change; the concentration of ownership of our common stock; fluctuations in the price of our common stock; our ability to fund or access the capital markets at attractive rates and terms and manage our growth, both organic growth as well as growth through other means, such as future acquisitions; inflation, interest rate, unemployment rate, and market and monetary fluctuations; the effects of potential new or increased tariffs, retaliatory tariffs and trade restrictions; the impact of international hostilities and geopolitical events; increased competition and its effect on the pricing of our products and services as well as our net interest rate spread and net interest margin; the loss of key employees; the effectiveness of our risk management strategies, including operational risks, including, but not limited to, client, employee, or fourth-party fraud and security breaches; and other risks described in this presentation and other filings we make with the Securities and Exchange Commission

(“SEC”). All forward-looking statements are necessarily only estimates of future results, and there can be no assurance that actual results will not differ materially from expectations. Therefore, you are cautioned not to place undue reliance on any forward-looking statements. Further, forward-looking statements included in this presentation are made only as of the date hereof, and we undertake no obligation to update or revise any forward-looking statements to reflect events or circumstances occurring after the date on which the statements are made or to reflect the occurrence of unanticipated events, unless required to do so under the federal securities laws. You should also review the risk factors described in the reports USCB Financial Holdings, Inc. has filed or will file with the SEC. Non-GAAP Financial Measures This presentation includes financial information determined by methods other than in accordance with generally accepted accounting principles (“GAAP”). This financial information includes certain operating performance measures. Management has included these non-GAAP financial measures because it believes these measures may provide useful supplemental information for evaluating the Company’s expectations and underlying performance trends. Further, management uses these measures in managing and evaluating the Company’s business and intends to refer to them in discussions about our operations and performance. Operating performance measures should be viewed in addition to, and not as an alternative to or substitute for, measures determined in accordance with GAAP, and are not necessarily comparable to non-GAAP measures that may be presented by other companies. Reconciliations of these non-GAAP measures to the most directly comparable GAAP measures can be found in the Non-GAAP financial measures reconciliation tables included in this presentation. 2

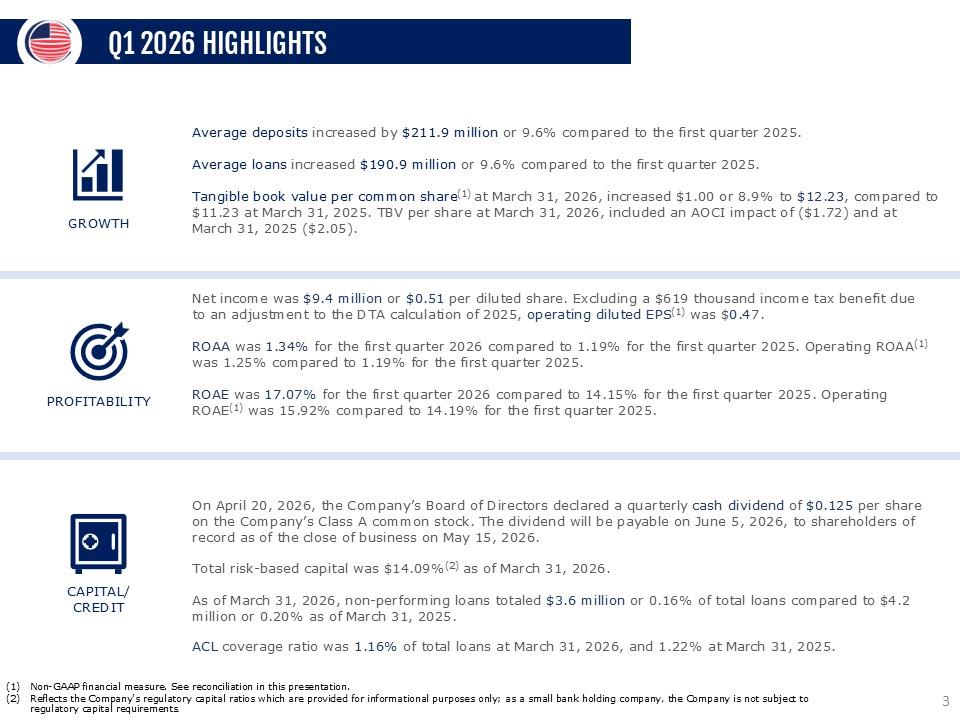

CAPITAL/ CREDIT PROFITABILITY GROWTH On April 20, 2026, the Company’s Board of Directors declared a quarterly cash dividend of $0.125 per share on the Company’s Class A common stock. The dividend will be payable on June 5, 2026, to shareholders of record as of the close of business on May 15, 2026. Total risk -based capital was $14.09%(2) as of March 31, 2026. As of March 31, 2026, non-performing loans totaled $3.6 million or 0.16% of total loans compared to $4.2 million or 0.20% as of March 31, 2025. ACL coverage ratio was 1.16% of total loans at March 31, 2026, and 1.22% at March 31, 2025. Average deposits increased by $211.9 million or 9.6% compared to the first quarter 2025. Average loans increased $190.9 million or 9.6% compared to the first quarter 2025. Tangible book value per common share(1) at March 31, 2026, increased $1.00 or 8.9% to $12.23, compared to $11.23 at March 31, 2025. TBV per share at March 31, 2026, included an AOCI impact of ($1.72) and at March 31, 2025 ($2.05). Q1 2026 HIGHLIGHTS Non-GAAP financial measure. See reconciliation in this presentation. Reflects the Company's regulatory capital ratios which are provided for informational purposes only; as a small bank holding company, the Company is not subject to regulatory capital requirements. Net income was $9.4 million or $0.51 per diluted share. Excluding a $619 thousand income tax benefit due to an adjustment to the DTA calculation of 2025, operating diluted EPS(1) was $0.47. ROAA was 1.34% for the first quarter 2026 compared to 1.19% for the first quarter 2025. Operating ROAA(1) was 1.25% compared to 1.19% for the first quarter 2025. ROAE was 17.07% for the first quarter 2026 compared to 14.15% for the first quarter 2025. Operating ROAE(1) was 15.92% compar ed to 14.19% for the first quarter 2025. 3

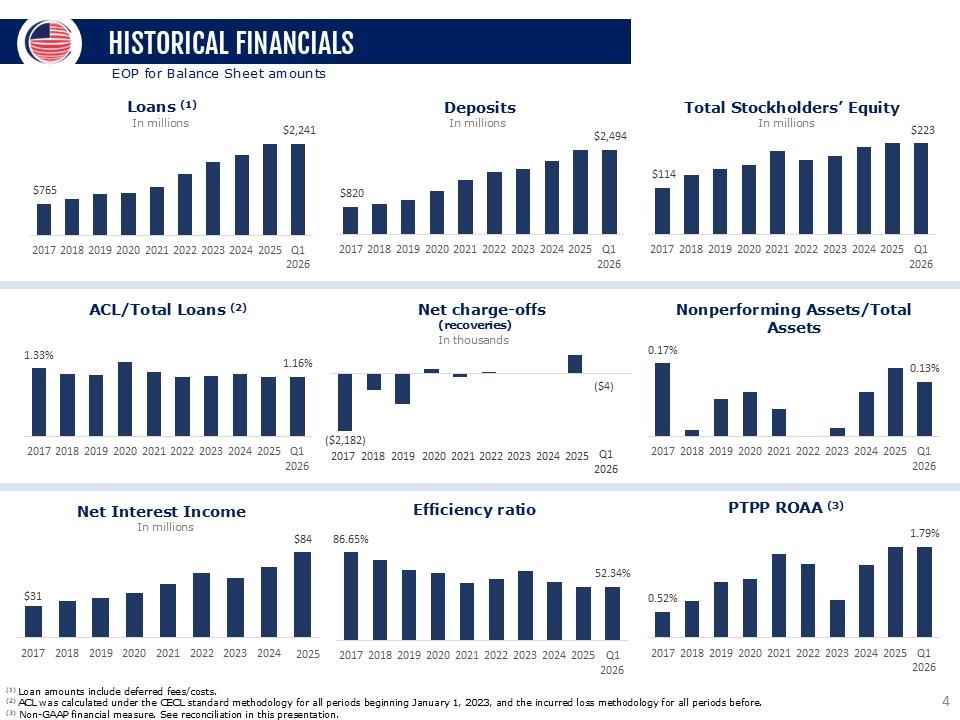

HISTORICAL FINANCIALS EOP for Balance Sheet amounts Loans (1) In millions $765 $2,241 2017 2018 2019 2020 2021 2022 2023 2024 2025 Q1 2026 Deposits In millions $820 $2,494 2017 2018 2019 2020 2021 2022 2023 2024 2025 Q1 2026 Total Stockholders’ Equity In millions $114 $223 2017 2018 2019 2020 2021 2022 2023 2024 2025 Q1 2026 ACL/Total Loans (2) 1.33% 1.16% 2017 2018 2019 2020 2021 2022 2023 2024 2025 Q1 2026 Net charge -offs (recoveries) In thousands ($21,872) ($4) 2017 2018 2019 2020 2021 2022 2023 2024 2025 Q1 2026 Nonperforming Assets/Total Assets 0.17% 0.13% 2017 2018 2019 2020 2021 2022 2023 2024 2025 Q1 2026

Net Interest Income

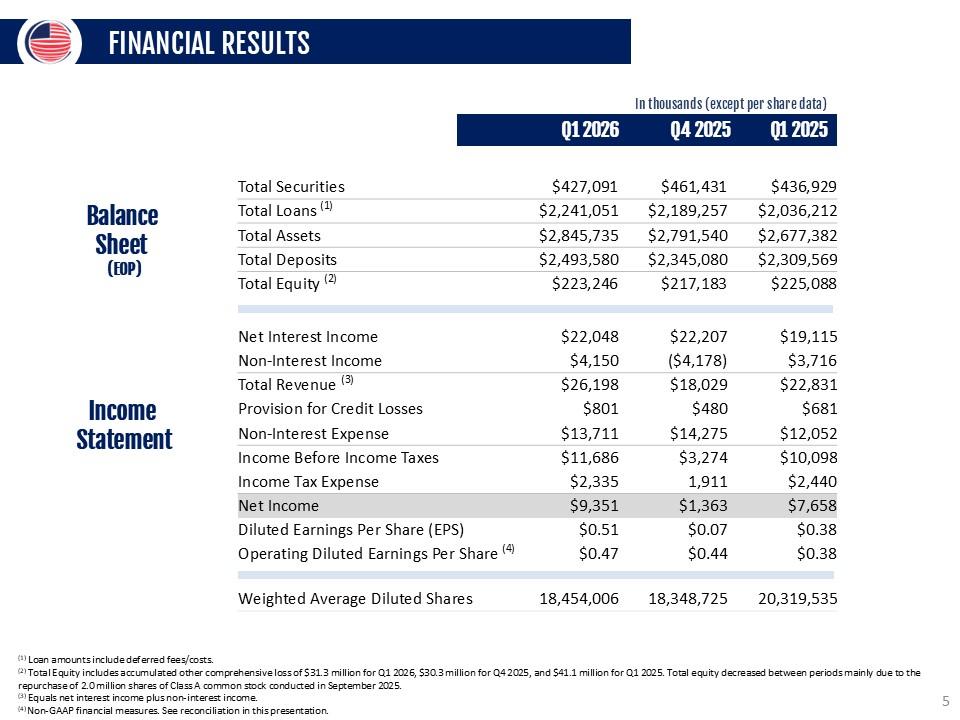

FINANCIAL RESULTS In thousands (except per share data) Balance Sheet (EOP) Income Statement Q1 2026 Q4 2025 Q1 2025 Total Securities $427,091 $461,431 $436,929 Total Loans (1) $2,241,051 $2,189,257 $2,036,212 Total Assets $2,845,735 $2,791,540 $2,677,382 Total Deposits $2,493,580 $2,345,080 $2,309,569 Total Equity (2) $223,246 $217,183 $225,088 Net Interest Income $22,048 $22,207 $19,115 Non-Interest Income $4,150 ($4,178) $3,716 Total Revenue (3) $26,198 $18,029 $22,831 Provision for Credit Losses $801 $480 $681 Non-Interest Expense $13,711 $14,275 $12,052 Income Before Income Taxes $11,686 $3,274 $10,098 Income Tax Expense $2,335 1,911 $2,440 Net Income $9,351 $1,363 $7,658 Diluted Earnings Per Share (EPS) $0.51 $0.07 $0.38 Operating Diluted Earnings Per Share (4) $0.47 $0.44 $0.38 Weighted Average Diluted Shares 18,454,006 18,348,725 20,319,535 (1) Loan amounts include deferred fees/costs. (2) Total Equity includes accumulated other comprehensive loss of $31.3 million for Q1 2026, $30.3 million for Q4 2025, and $41.1 million for Q1 2025. Total equity decreased between periods mainly due to the repurchase of 2.0 million shares of Class A common stock conducted in September 2025. (3) Equals net interest income plus non-interest income. (4) Non-GAAP financial measures. See reconciliation in this presentation. 5

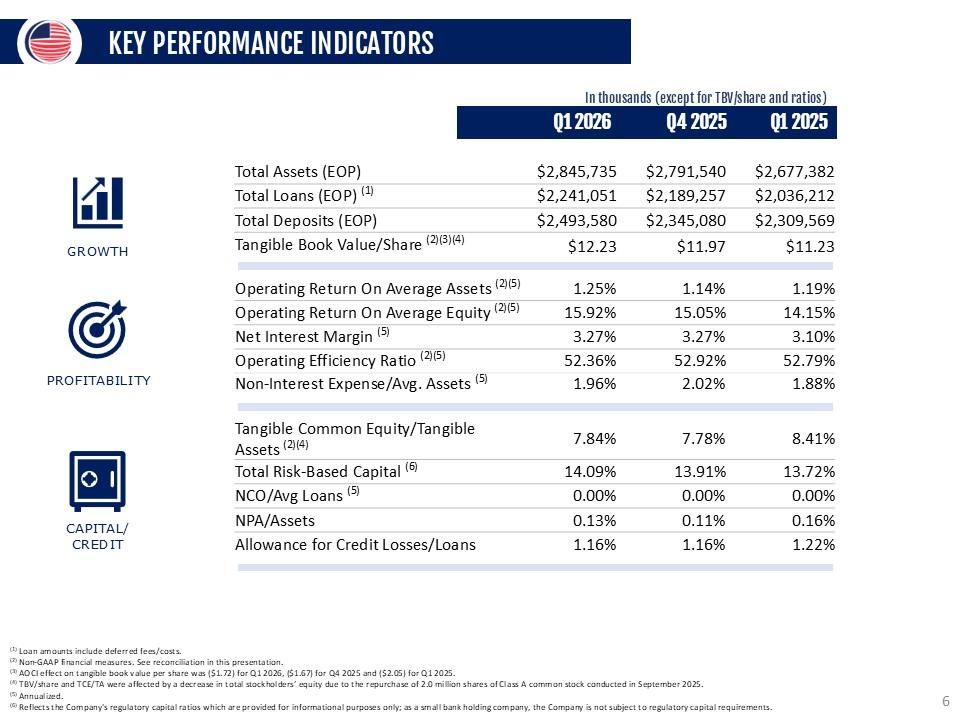

KEY PERFORMANCE INDICATORS In thousands (except for TBV/share and ratios) Q1 2026 Q4 2025 Q1 2025 Total Assets (EOP) $2,845,735 $2,791,540 $2,677,382 Total Loans (EOP) (1) $2,241,051 $2,189,257 $2,036,212 Total Deposits (EOP) $2,493,580 $2,345,080 $2,309,569 Tangible Book Value/Share (2)(3)(4) $12.23 $11.97 $11.23 Operating Return On Average Assets (2)(5) 1.25% 1.14% 1.19% Operating Return On Average Equity (2)(5) 15.92% 15.05% 14.15% Net Interest Margin (5) 3.27% 3.27% 3.10% Operating Efficiency Ratio (2)(5) 52.36% 52.92% 52.79% Non-Interest Expense/Avg. Assets (5) 1.96% 2.02% 1.88% Tangible Common Equity/Tangible Assets (2)(4) 7.84% 7.78% 8.41% Total Risk-Based Capital (6) 14.09% 13.91% 13.72% NCO/Avg Loans (5) 0.00% 0.00% 0.00% NPA/Assets 0.13% 0.11% 0.16% Allowance for Credit Losses/Loans 1.16% 1.16% 1.22% (1) Loan amounts include deferred fees/costs. (2) Non-GAAP financial measures. See reconciliation in this presentation. (3) AOCI effect on tangible book value per share was ($1.72) for Q1 2026, ($1.67) for Q4 2025 and ($2.05) for Q1 2025. (4) TBV/share and TCE/TA were affected by a decrease in total stockholders’ equity due to the repurchase of 2.0 million shares of Class A common stock conducted in September 2025. (5) Annualized. (6) Reflects the Company's regulatory capital ratios which are provided for informational purposes only; as a small bank holding company, the Company is not subject to regulatory capital requirements. 6

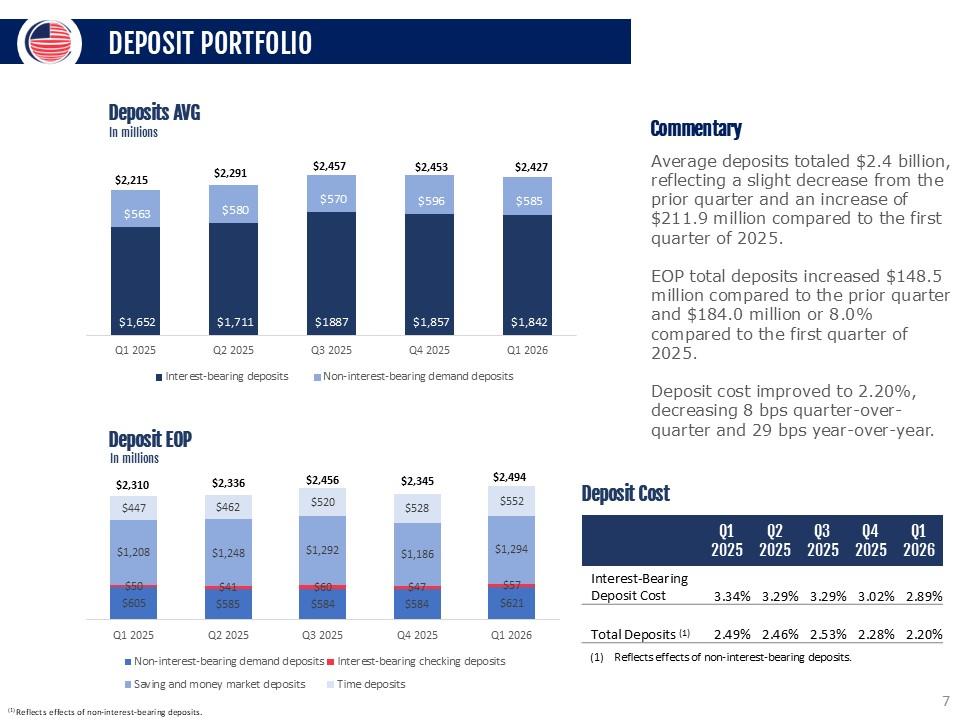

DEPOSIT PORTFOLIO Deposits AVG In millions $2,215 $2,291 $2,457 $2,453 $2,427 $563 $580 $570 $569 $585 $1,652 $1,711 $1,887 $1,857 $1,842 Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Interest-bearing deposits Non-interest-bearing demand deposit Deposit EOP In millions $2,310 $2,336 $2,456 $2,345 $2,494 $447 $462 $520 $528 $552 $1,208 $1,248 $1,292 $1,186 $1,294 $50 $41 $60 $47 $57 $605 $585 $584 $584 $621 Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Non-interest-bearing demand deposits Interest-bearing checking deposits Saving and money market deposits Time deposits Commentary Average deposits totaled $2.4 billion, reflecting a slight decrease from the prior quarter and an increase of $211.9 million compared to the first quarter of 2025. EOP total deposits increased $148.5 million compared to the prior quarter and $184.0 million or 8.0% compared to the first quarter of 2025. Deposit cost improved to 2.20%, decreasing 8 bps quarter-over-quarter and 29 bps year-over-year. in this slide the Deposits AVG totals must be updated manually Same goes for the red bps math Deposit Cost Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Interest-Bearing Deposit Cost 3.34% 3.29% 3.29% 3.02% 2.89% Total Deposits (1) 2.49% 2.46% 2.53% 2.28% 2.20% (1) Reflects effects of non-interest-bearing deposits. 7

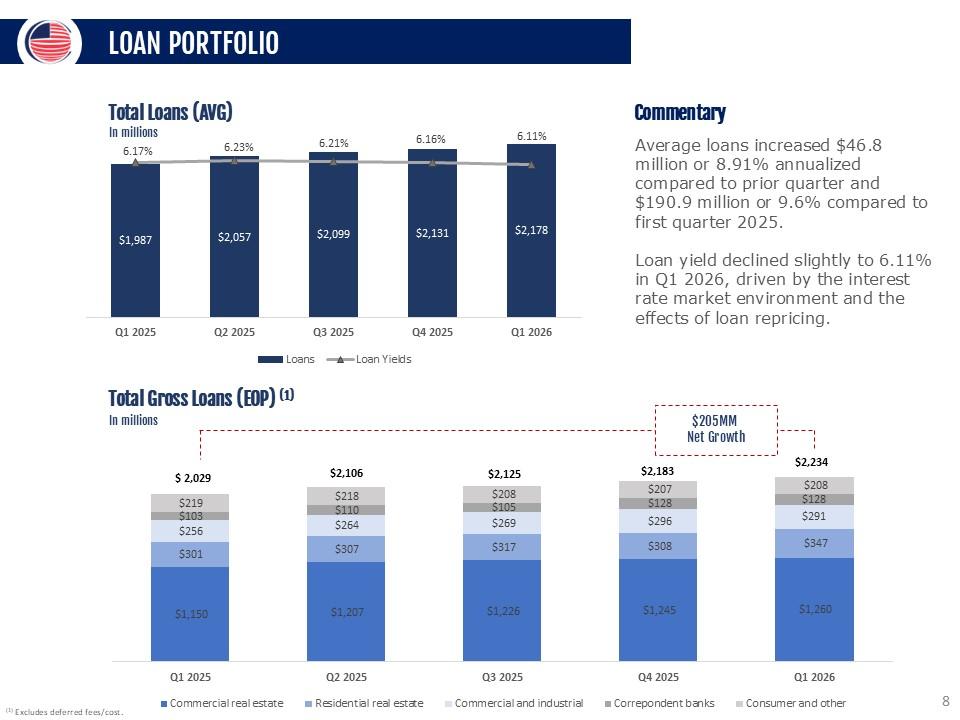

LOAN PORTFOLIO Total Loans (AVG) In millions 6.17% 6.23% 6.21% 6.16% 6.11% $1,987 $2,057 $2,099 $2,131 $2,178 Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Loans Loan Yields Total Gross Loans (EOP) (1) In millions $2,029 $2,106 $2,125 $2,183 $2,234 $219 $218 $208 $207 $208 $103 $110 $105 $128 $128 $256 $264 $269 $296 $291 $301 $307 $317 $308 $347 $1,150 $1,207 $1,226 $1,245 $1,260 Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Commercial real estate Residential rea Commercial and industrial Correspondent banks Consumer and other Commentary Average loans increased $46.8 million or 8.91% annualized compared to prior quarter and $190.9 million or 9.6% compared to first quarter 2025. Loan yield declined slightly to 6.11% in Q1 2026, driven by the interest rate market environment and the effects of loan repricing. (1) Excludes deferred fees/cost. 8

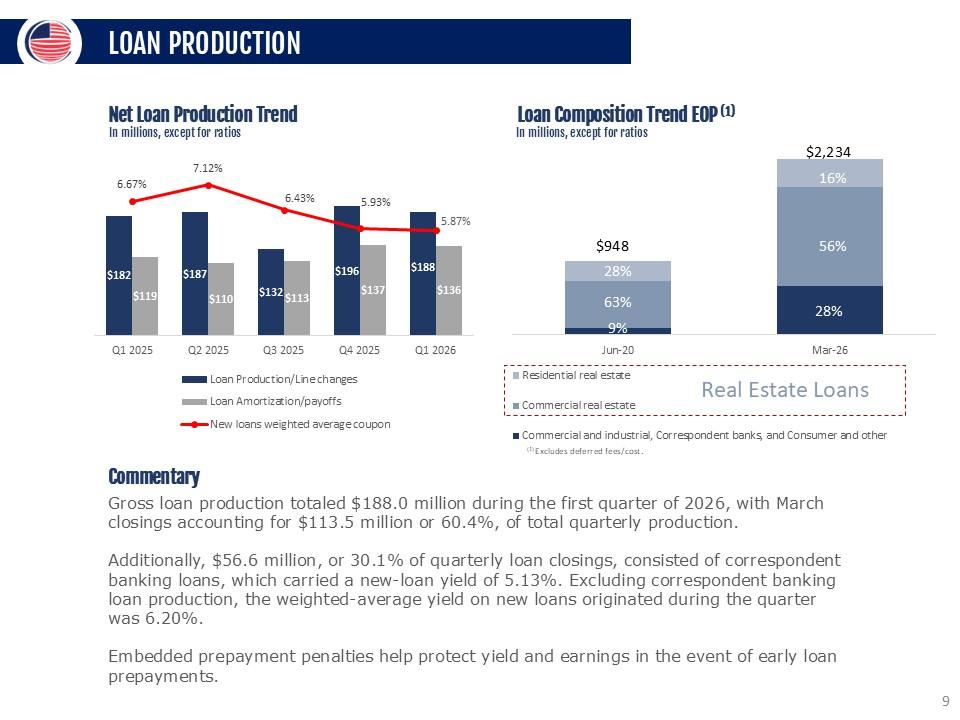

LOAN PRODUCTION In millions, except for ratios 6.67% 7.12% 6.43% 5.93% 5.87% $182 $119 $187 $110 $132 $113 $196 $137 $188 $136 Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Loan Production/Line change Loan Amortization/payoffs New loans weighted average coupon Net Loan Production Trend Loan Composition Trend EOP (1) In millions, except for ratios $948 $2,234 28% 16% 63% 56% 9% 28% Jun-20 Mar-26 Residential real estate Commercial real estate Real Estate Loans Commentary Gross loan production totaled $188.0 million during the first quarter of 2026, with March closings accounting for $113.5 million or 60.4%, of total quarterly production. Additionally, $56.6 million, or 30.1% of quarterly loan closings, consisted of correspondent banking loans, which carried a new‑loan yield of 5.13%. Excluding correspondent banking loan production, the weighted‑average yield on new loans originated during the quarter was 6.20%. Embedded prepayment penalties help protect yield and earnings in the event of early loan prepayments. (1) Excludes deferred fees/cost. 9

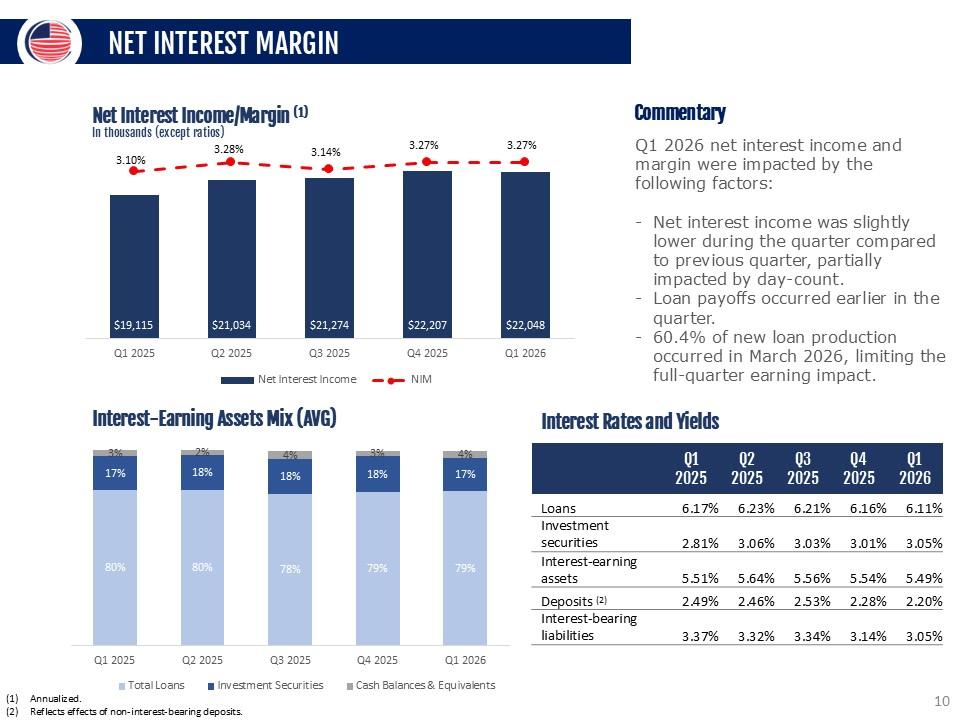

NET INTEREST MARGIN Net Interest Income/Margin (1) In thousands (except ratios) 3.10% 3.28% 3.14% 3.27% 3.27% $19,115 $21,034 $21,274 $22,207 $22,048 Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Net Interest Income NIM Interest-Earning Assets Mix (AVG) 3% 2% 4% 3% 4% 17% 18% 18% 18% 17% 80% 80% 78% 79% 79% Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Total Loans Investment Securities Cash Balances & Equivalents Commentary Q1 2026 net interest income and margin were impacted by the following factors: Net interest income was slightly lower during the quarter compared to previous quarter, partially impacted by day-count. Loan payoffs occurred earlier in the quarter. 60.4% of new loan production occurred in March 2026, limiting the full-quarter earning impact. Interest Rates and Yields Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Loans 6.17% 6.23% 6.21% 6.16% 6.11% Investment securities 2.81% 3.06% 3.03% 3.01% 3.05% Interest-earning assets 5.51% 5.64% 5.56% 5.54% 5.49% Deposits (2) 2.49% 2.46% 2.53% 2.28% 2.20% Interest -bearing liabilities 3.37% 3.32% 3.34% 3.14% 3.05% (1) Annualized. (2) Reflects effects of non-interest-bearing deposits. 10

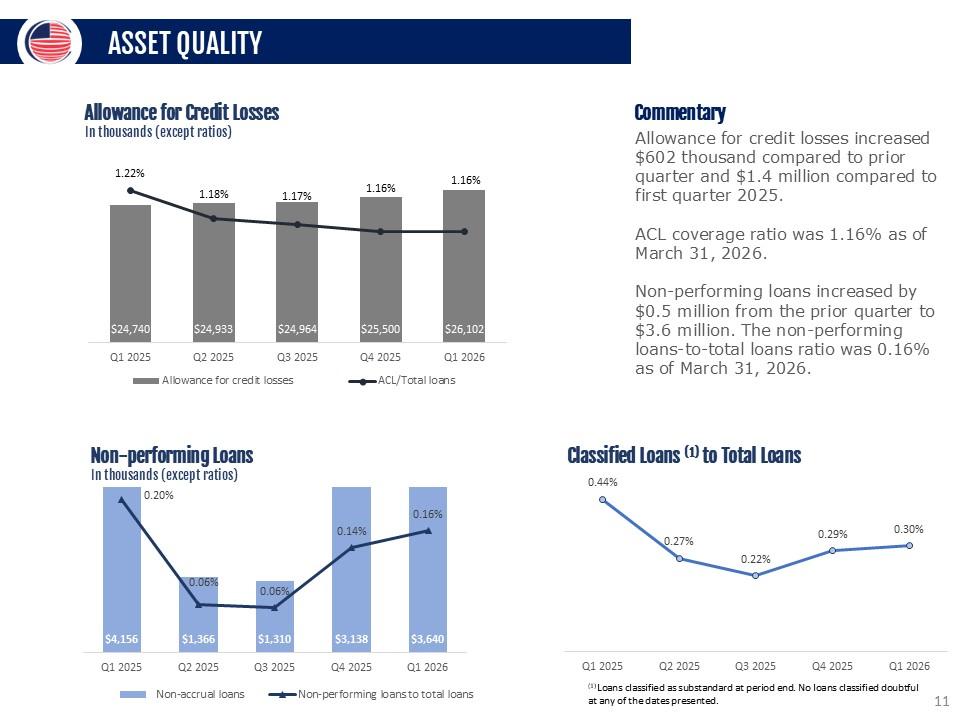

ASSET QUALITY Allowance for Credit Losses In thousands (except ratios) 1.22% 1.18% 1.17% 1.16% 1.16% $24,740 $24,933 $24,964 $25,500 $26,102 Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Allowance for credit losses Non-performing Loans In thousands (except ratios) 0.20% 0.06% 0.06% 0.14% 0.16% $4,156 $1,366 $1,310 $3,138 $3,640 Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Non-accrual loans Non-performing loans to total loans Commentary Allowance for credit losses increased $602 thousand compared to prior quarter and $1.4 million compared to first quarter 2025. ACL coverage ratio was 1.16% as of March 31, 2026. Non‑performing loans increased by $0.5 million from the prior quarter to $3.6 million. The non‑performing loans‑to‑total loans ratio was 0.16% as of March 31, 2026. Classified Loans (1) to Total Loans 0.44% 0.27% 0.22% 0.29% 0.30% Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 (1) Loans classified as substandard at period end. No loans classified doubtful at any of the dates presented. 11

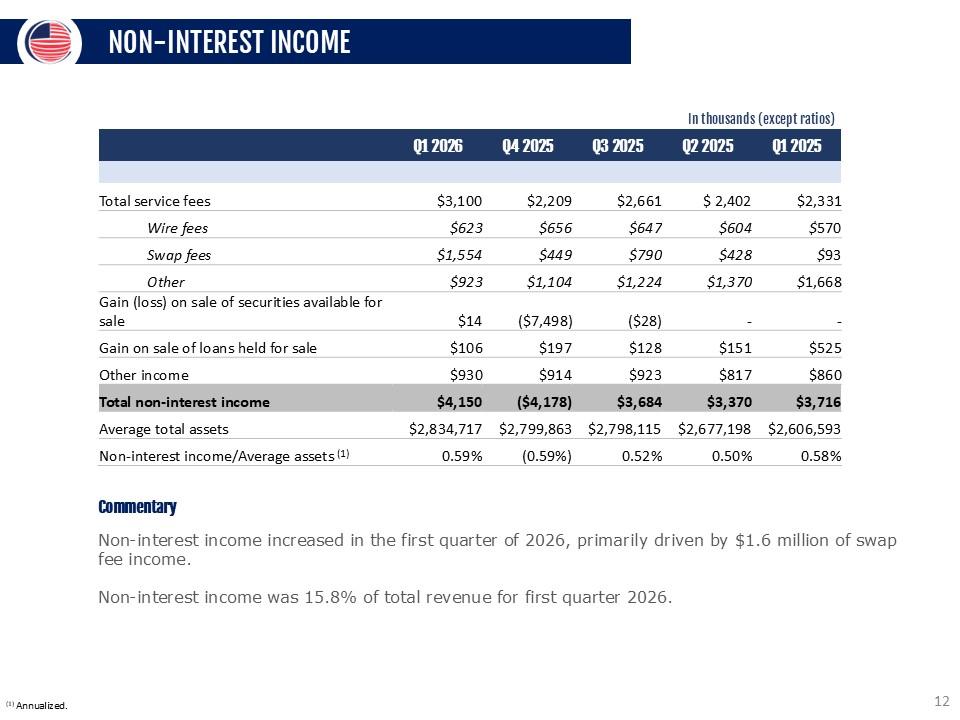

NON-INTEREST INCOME In thousands (except ratios) Q1 2026 Q4 2025 Q3 2025 Q2 2025 Q1 2025 Total service fees $3,100 $2,209 $2,661 $ 2,402 $2,331 Wire fees $623 $656 $647 $604 $570 Swap fees $1,554 $449 $790 $428 $93 Other $923 $1,104 $1,224 $1,370 $1,668 Gain (loss) on sale of securities available for sale $14 ($7,498) ($28) - - Gain on sale of loans held for sale $106 $197 $128 $151 $525 Other income $930 $914 $923 $817 $860 Total non-interest income $4,150 ($4,178) $3,684 $3,370 $3,716 Average total assets $2,834,717 $2,799,863 $2,798,115 $2,677,198 $2,606,593 Non-interest income/Average assets (1) 0.59% (0.59%) 0.52% 0.50% 0.58% Commentary Non-interest income increased in the first quarter of 2026, primarily driven by $1.6 million of swap fee income. Non-interest income was 15.8% of total revenue for first quarter 2026. (1) Annualized. 12

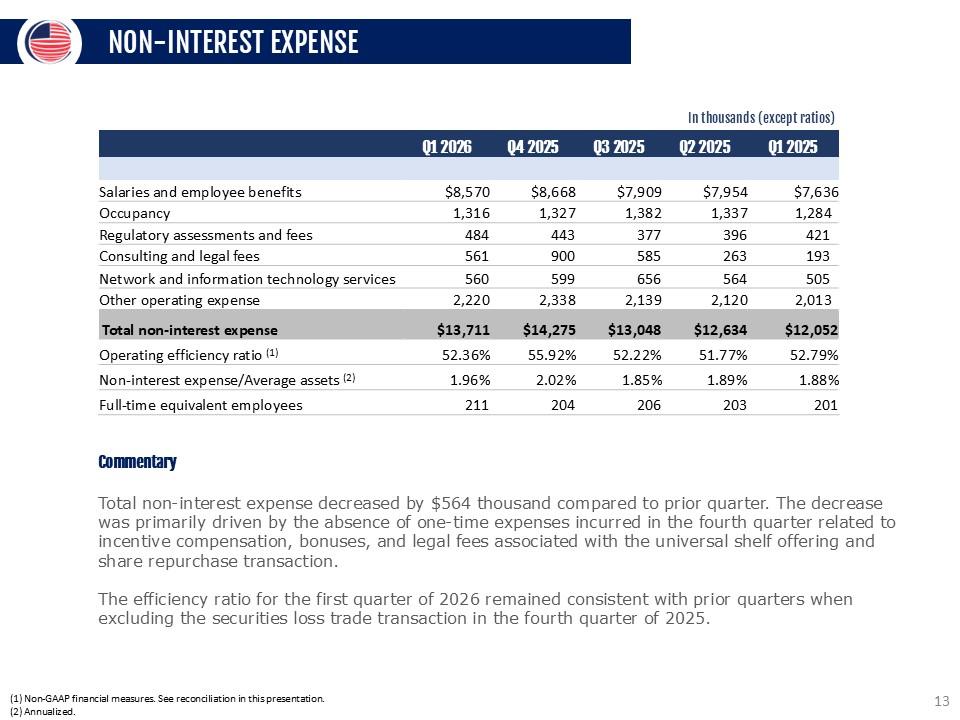

NON-INTEREST EXPENSE In thousands (except ratios) Q1 2026 Q4 2025 Q3 2025 Q2 2025 Q1 2025 Salaries and employee benefits $8,570 $8,668 $7,909 $7,954 $7,636 Occupancy 1,316 1,327 1,382 1,337 1,284 Regulatory assessments and fees 484 443 377 396 421 Consulting and legal fees 561 900 585 263 193 Network and information technology services 560 599 656 564 505 Other operating expense 2,220 2,338 2,139 2,120 2,013 Total non-interest expense $13,711 $14,275 $13,048 $12,634 $12,052 Operating efficiency ratio (1) 52.36% 55.92% 52.22% 51.77% 52.79% Non -interest expense/Average assets (2) 1.96% 2.02% 1.85% 1.89% 1.88% Full-time equivalent employees 211 204 206 203 201 Commentary Total non-interest expense decreased by $564 thousand compared to prior quarter. The decrease was primarily driven by the absence of one-time expenses incurred in the fourth quarter related to incentive compensation, bonuses, and legal fees associated with the universal shelf offering and share repurchase transaction. The efficiency ratio for the first quarter of 2026 remained consistent with prior quarters when excluding the securities loss trade transaction in the fourth quarter of 2025. (1) Non-GAAP financial measures. See reconciliation in this presentation. (2) Annualized. 13

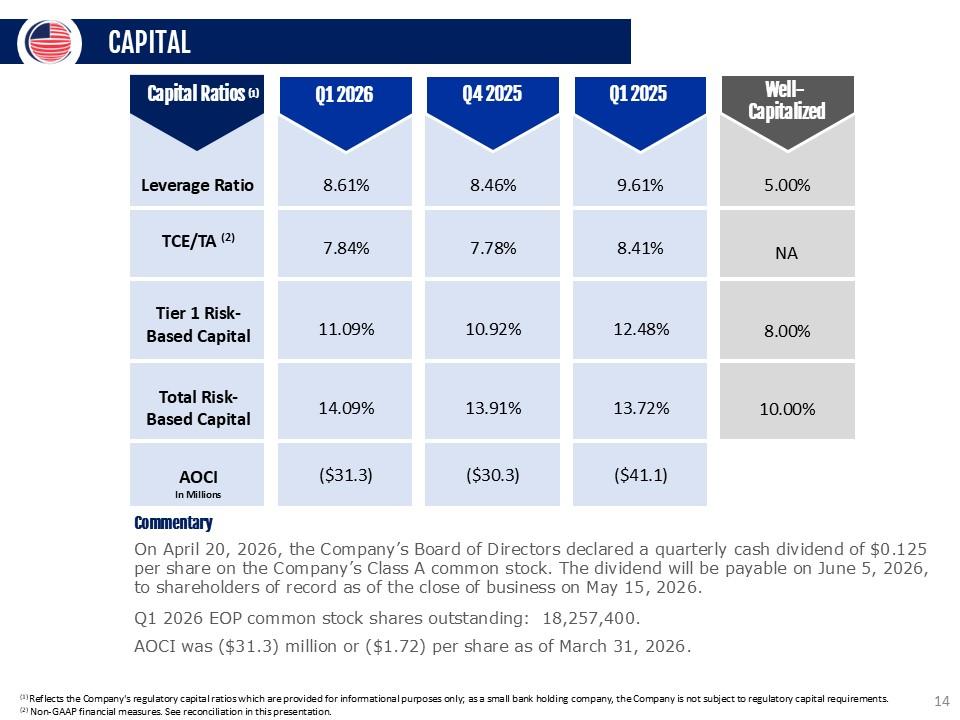

CAPITAL Capital Ratios (1) Q3 2025 Q1 2025 Well- Capitalized Leverage Ratio TCE/TA (2) Tier 1 Risk-Based Capital Total Risk-Based Capital AOCI In Millions 8.46% 7.78% 10.92% 13.91% ($30.3) 9.61% 8.41% 12.48% 13.72% ($41.1) 5.00% NA 8.00% 10.00% Q4 2025 Commentary On April 20, 2026, the Company’s Board of Directors declared a quarterly cash dividend of $0.125 per share on the Company’s Class A common stock. The dividend will be payable on June 5, 2026, to shareholders of record as of the close of business on May 15, 2026. Q1 2026 EOP common stock shares outstanding: 18,257,400. AOCI was ($31.3) million or ($1.72) per share as of March 31, 2026. 8.61% 7.84% 11.09% 14.09% ($31.3) Q1 2026 (1) Reflects the Company's regulatory capital ratios which are provided for informational purposes only; as a small bank holding company, the Company is not subject to regulatory capital requirements. (2) Non-GAAP financial measures. See reconciliation in this presentation. 14

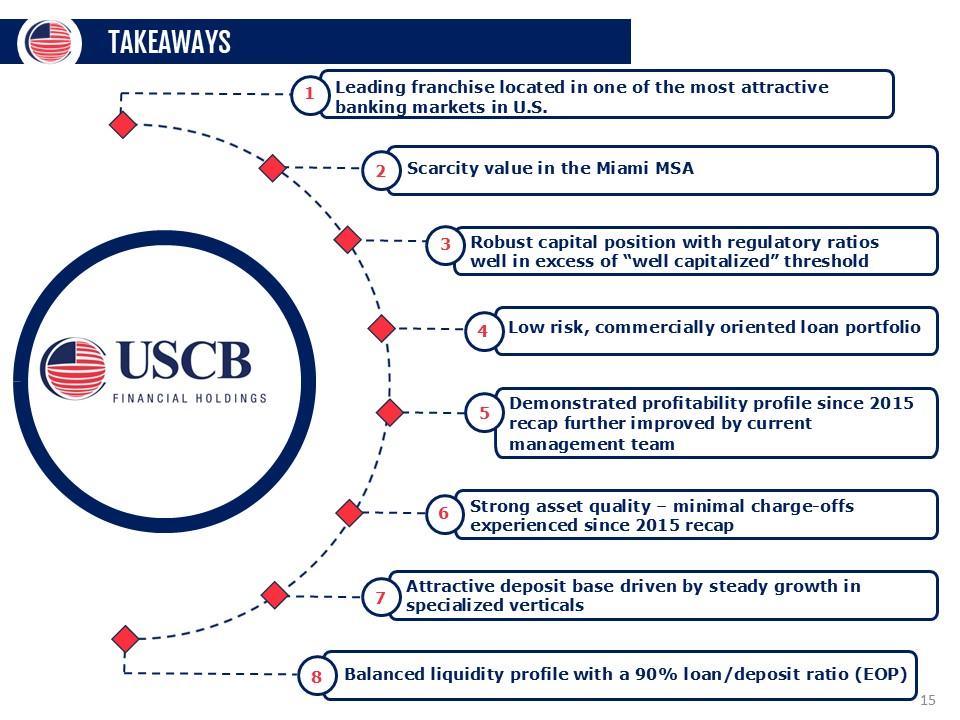

USCB FINANCIAL HOLDINGS TAKEAWAYS 1. Leading franchise located in one of the most attractive banking markets in U.S. 2. Scarcity value in the Miami MSA 3. Robust capital position with regulatory ratios well in excess of “well capitalized” threshold 4. Low risk, commercially oriented loan portfolio 5. Demonstrated profitability profile since 2015 recap further improved by current management team 6. Strong asset quality – minimal charge -offs experienced since 2015 recap 7. Attractive deposit base driven by steady growth in specialized verticals 8. Balanced liquidity profile with a 90% loan/deposit ratio (EOP) 15

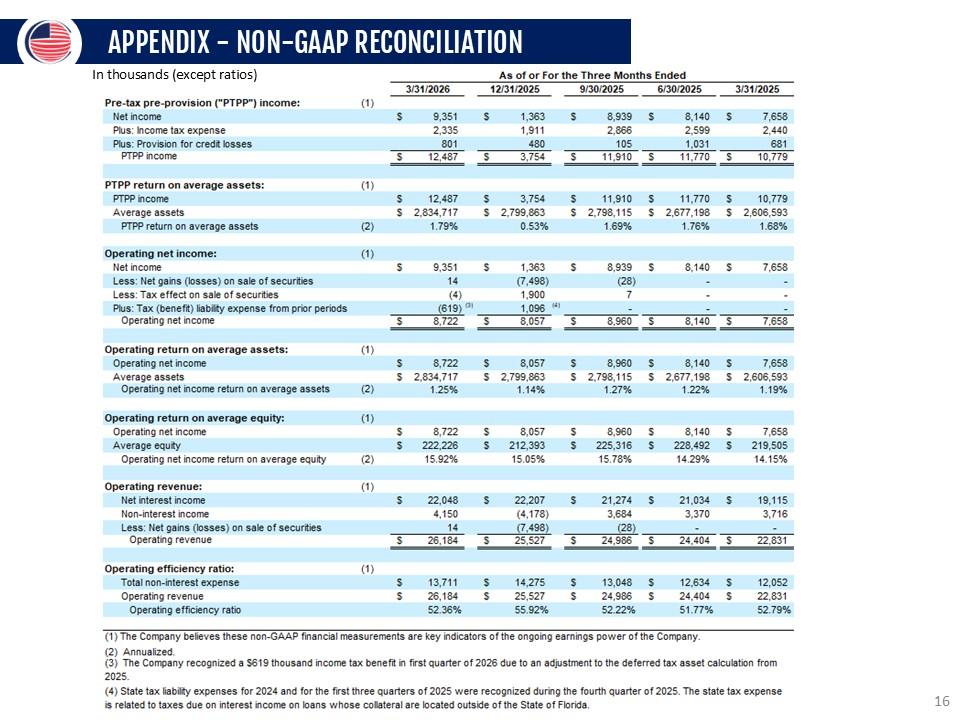

APPENDIX - NON-GAAP RECONCILIATION In thousands (except ratios) As of or For the Three Months Ended 3/31/2026 12/31/2025 9/30/2025 6/30/2025 3/31/2025 Pre-tax pre-provision ("PTPP") income: (1) Net income s 9,351 $ 1,363 $ 8,939 s 8,140 s 7,658 Plus: Income tax expense 2,335 1,911 2,866 2,599 2,440 Plus: Provision for credit losses 801 480 105 1,031 681 PTPP income S—12,487 S 3,754 S11,910 S 11,770 S 10,779 PTPP return on average assets: (1) PTPP income 2sammr, eoig,ge s 12,487 c D oo s 7*7 s 3,754 S 2,799,863 0.53% s 11,910 S 2,798,115 1.69% s 11,770 s 2,677,198 1.76% s 10,779 s 2,606,593 1.68% Average DepositsPTPP return on average assets (2) 1.79% Operating net income: (1) Net income S 9,351 S 1,363 S 8,939 S 8,140 S 7,658 Less: Net gains (losses) on sale of securities 14 (7,498) (28) - - Less: Tax effect on sale of securities (4) 1,900 7 - - Plus: Tax (beneft) fability expense from prior periods (619)” 1,096" - - - Operating net income s 8,722 S 8,057 S 8,960 s 8,140 s 7,658 Operating return on average assets: Operating net income Average assets (1) s 8,722 $ 2,834,717 s 8,057 S 2,799,863 s 8,960 $ 2,798,115 s 8,140 s 2,677,198 s 7,658 s 2,606,593 Operating net income return on average assets (2) 1.25% 1.14% 1.27% 1.22% 1.19% Operating return on average equity: Operating net income (1) s 8,722 s 8,057 s 8,960 s 8,140 s 7,658 Average equity Operating net income return on average equity (2) S 222,226 15.92% s 212,393 15.05% s 225,316 15.78% S 228,492 14.29% S 219,505 14.15% Operating revenue: (1) Net interest income S 22,048 S 22,207 S 21,274 S 21,034 S 19,115 Non-interest income 4,150 (4,178) 3,684 3,370 3,716 Less: Net gains (losses) on sale of securities 14 (7.498) (28) - - Operating revenue s 26,184 s 25,527 s 24,986 s 24,404 s 22,831 Operating efficiency ratio: (1) Total non-interest expense s 13,711 s 14,275 s 13,048 s 12,634 s

12,052 Operating revenue S 26,184 $ 25,527 $ 24,986 S 24,404 S 22,831 Operating efficiency ratio 52.36% 55.92% 52.22% 51.77% 52.79% (1 ) The Company beleves these non-GAAP financial measurements are key indicators of the ongoing earnings power of the Company. 2. Annualized. 3. The Company recognized a $61 9 thousand income tax benefit in first quarter of 2026 due to an adjustment to the deferred tax asset calculation from 2025. 4. State tax fability expenses for 2024 and for the first three quarters of 2025 were recognized during the fourth quarter of 2025. The state tax expense is related to taxes due on interest income on loans whose collateral are located outside of the State of Florida. 16

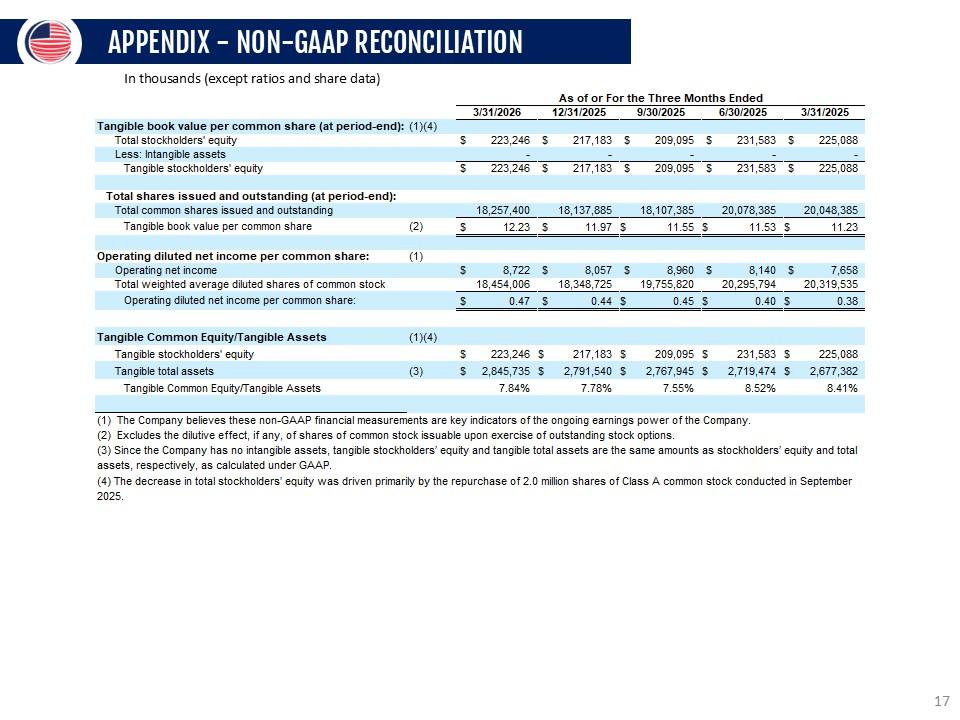

APPENDIX - NON-GAAP RECONCILIATION In thousands (except ratios and share data) As of or For the Three Months Ended 3/31/2026 12/31/2025 9/30/2025 6/30/2025 3/31/2025 Tangible book value per common share (at period-end): (1)(4) Total stockholders' equity s 223,246 s 217,183 s 209,095 s 231,583 s 225,088 Less: Intangible assets - - - - - Tangible stockholders' equity s 223,246 s 217,183 s 209,095 s 231,583 s 225,088 Total shares issued and outstanding (at period-end): Total common shares issued and outstanding 18,257,400 18,137,885 18,107,385 20,078,385 20,048,385 Tangible book value per common share (2) s 12.23 $ 11.97 $ 11.55 $ 11.53 $ 11.23 Operating diluted net income per common share: (1) Operating net income s 8,722 s 8,057 s 8,960 s 8,140 s 7,658 Total weighted average diluted shares of common stock 18,454,006 18,348,725 19,755,820 20,295,794 20,319,535 Operating diluted net income per common share: s 0.47 s 0.44 s 0.45 s 0.40 s 0.38 Tangible Common Equity Tangible Assets (1)(4) Tangible stockholders' equity s 223,246 s 217,183 s 209,095 s 231,583 s 225,088 Tangible total assets (3) s 2,845,735 s 2,791,540 s 2,767,945 s 2,719,474 s 2,677,382 Tangible Common Equity/Tangible Assets 7.84% 7.78% 7.55% 8.52% 8.41% (1 ) The Company believes these non-GAAP financial measurements are key indicators of the ongoing earnings power of the Company. 2. Excludes the dilutive effect, if any, of shares of common stock issuable upon exercise of outstanding stock options. 3. Since the Company has no intangible assets, tangible stockholders equity and tangible total assets are the same amounts as stockholders equity and total assets, respectively, as calculated under GAAP. 4. The decrease in total stockholders equity was driven primarily by the repurchase of 2.0 million shares of Class A common stock conducted in September 2025. 17

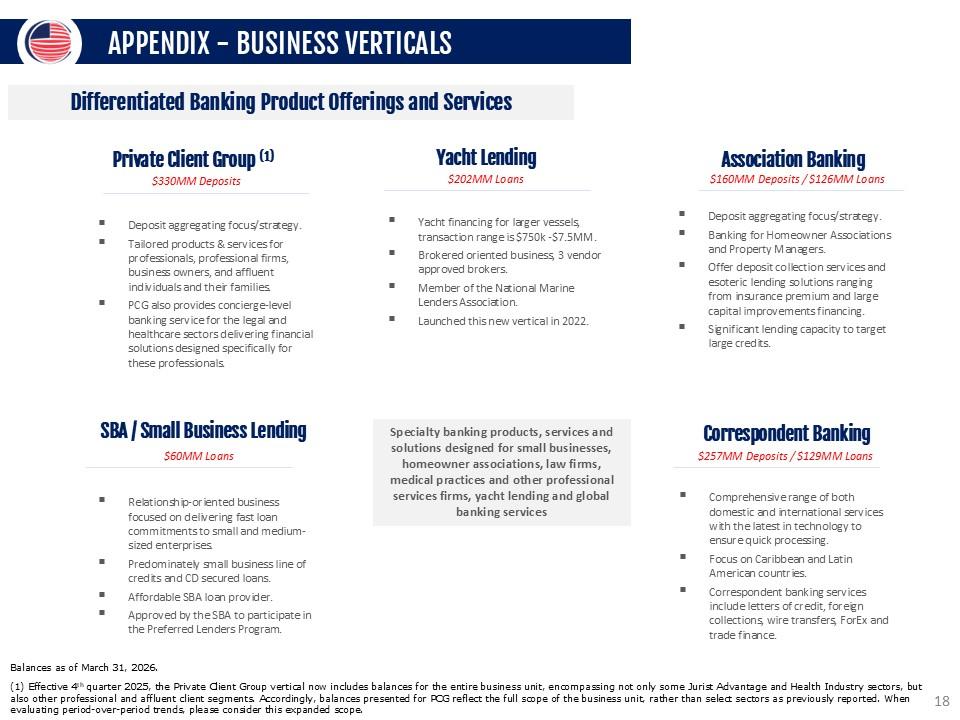

APPENDIX - BUSINESS VERTICALS in this slide the % of loan comp must be updated manually Private Client Group (1) $330MM Deposits Association Banking $160MM Deposits / $126MM Loans Deposit aggregating focus/strategy. Tailored products & services for professionals, professional firms, business owners, and affluent individuals and their families. PCG also provides concierge-level banking service for the legal and healthcare sectors delivering financial solutions designed specifically for these professionals. Deposit aggregating focus/strategy. Banking for Homeowner Associations and Property Managers. Offer deposit collection services and esoteric lending solutions ranging from insurance premium and large capital improvements financing. Significant lending capacity to target large credits. Yacht Lending $202MM Loans Yacht financing for larger vessels, transaction range is $750k -$7.5MM. Brokered oriented business, 3 vendor approved brokers. Member of the National Marine Lenders Association. Launched this new vertical in 2022. Balances as of March 31, 2026. Differentiated Banking Product Offerings and Services Specialty banking products, services and solutions designed for small businesses, homeowner associations, law firms, medical practices and other professional services firms, yacht lending and global banking services Correspondent Banking $257MM Deposits / $129MM Loans Comprehensive range of both domestic and international services with the latest in technology to ensure quick processing. Focus on Caribbean and Latin American countries. Correspondent banking services include letters of credit, foreign collections, wire transfers, ForEx and trade finance. SBA / Small Business Lending $60MM Loans Relationship-oriented business focused on delivering fast loan commitments to small and medium-sized enterprises. Predominately small business line of

credits and CD secured loans. Affordable SBA loan provider. Approved by the SBA to participate in the Preferred Lenders Program. (1) Effective 4th quarter 2025, the Private Client Group vertical now includes balances for the entire business unit, encompassing not only some Jurist Advantage and Health Industry sectors, but also other professional and affluent client segments. Accordingly, balances presented for PCG reflect the full scope of the business unit, rather than select sectors as previously reported. When evaluating period-over-period trends, please consider this expanded scope. 18

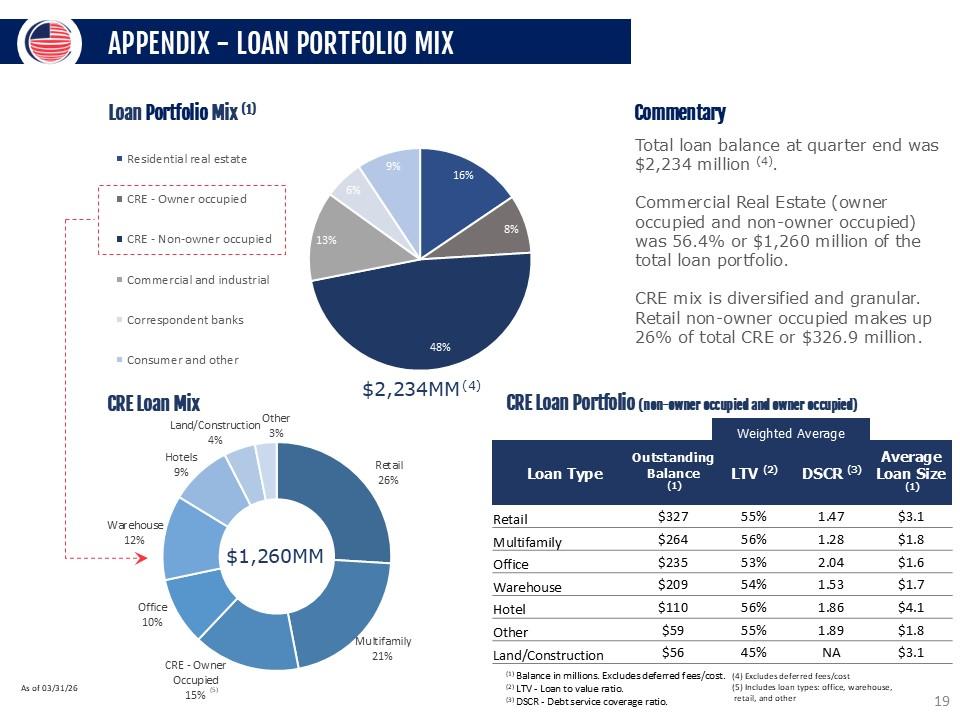

APPENDIX - LOAN PORTFOLIO MIX Loan Portfolio Mix (1) As of 03/31/26 CRE Loan Portfolio (non-owner occupied and owner occupied) (5) in this slide the CRE Loan Mix sum and Loan Portfolio Mix sum must be updated manually $1,260MM CRE Loan Mix $2,234MM (4) Commentary Total loan balance at quarter end was $2,234 million (4). Commercial Real Estate (owner occupied and non-owner occupied) was 56.4% or $1,260 million of the total loan portfolio. CRE mix is diversified and granular. Retail non-owner occupied makes up 26% of total CRE or $326.9 million . (1) Balance in millions. Excludes deferred fees/cost. (2) LTV - Loan to value ratio. (3) DSCR - Debt service coverage ratio. (4) Excludes deferred fees/cost (5) Includes loan types: office, warehouse, retail, and other 19

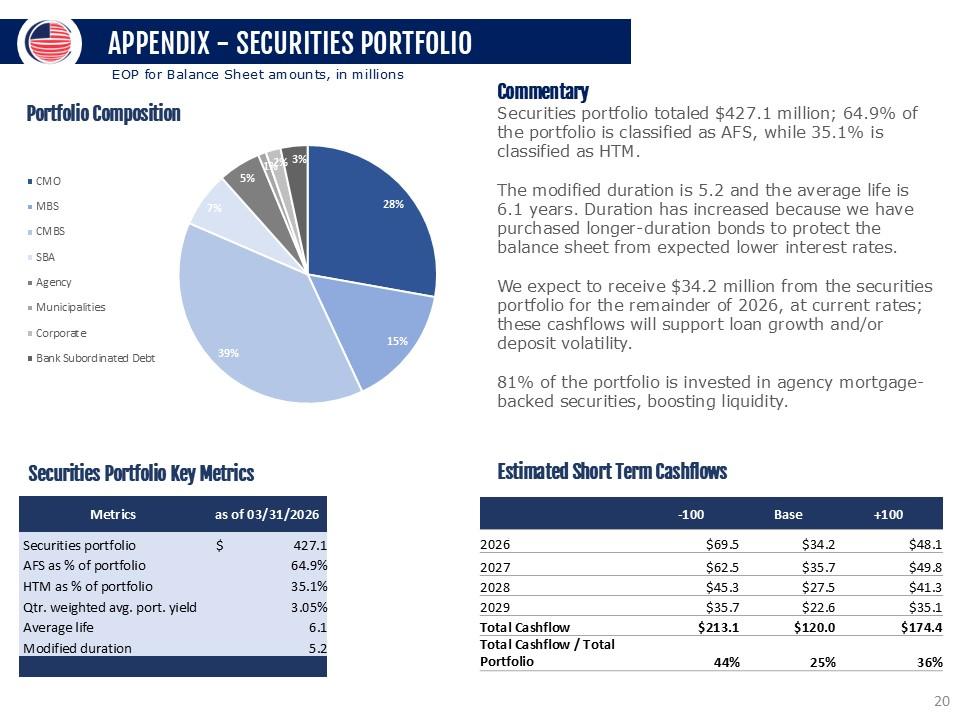

APPENDIX - SECURITIES PORTFOLIO Portfolio Composition CMO MBS CMBS SBA Agency Municipalities Corporate Bank Subordinated Debt 3% 28% 15% 39% 7% 5% 1% 2% Commentary Securities portfolio totaled $427.1 million; 64.9% of the portfolio is classified as AFS, while 35.1% is classified as HTM. The modified duration is 5.2 and the average life is 6.1 years. Duration has increased because we have purchased longer-duration bonds to protect the balance sheet from expected lower interest rates. We expect to receive $34.2 million from the securities portfolio for the remainder of 2026, at current rates; these cashflows will support loan growth and/or deposit volatility. 81% of the portfolio is invested in agency mortgage-backed securities, boosting liquidity. EOP for Balance Sheet amounts, in millions Securities Portfolio Key Metrics Metrics as of 03/31/2026 Securities portfolio $ 427.1 AFS as % of portfolio 64.9% HTM as % of portfolio 35.1% Qtr. weighted avg. port. yield 3.05% Average life 6.1 Modified duration 5.2 Estimated Short Term Cashflows -100 Base +100 2026 $69.5 $34.2 $48.1 2027 $62.5 $35.7 $49.8 2028 $45.3 $27.5 $41.3 2029 $35.7 $22.6 $35.1 Total Cashflow $213.1 $120.0 $174.4 Total Cashflow / Total Portfolio 44% 25% 36% 20

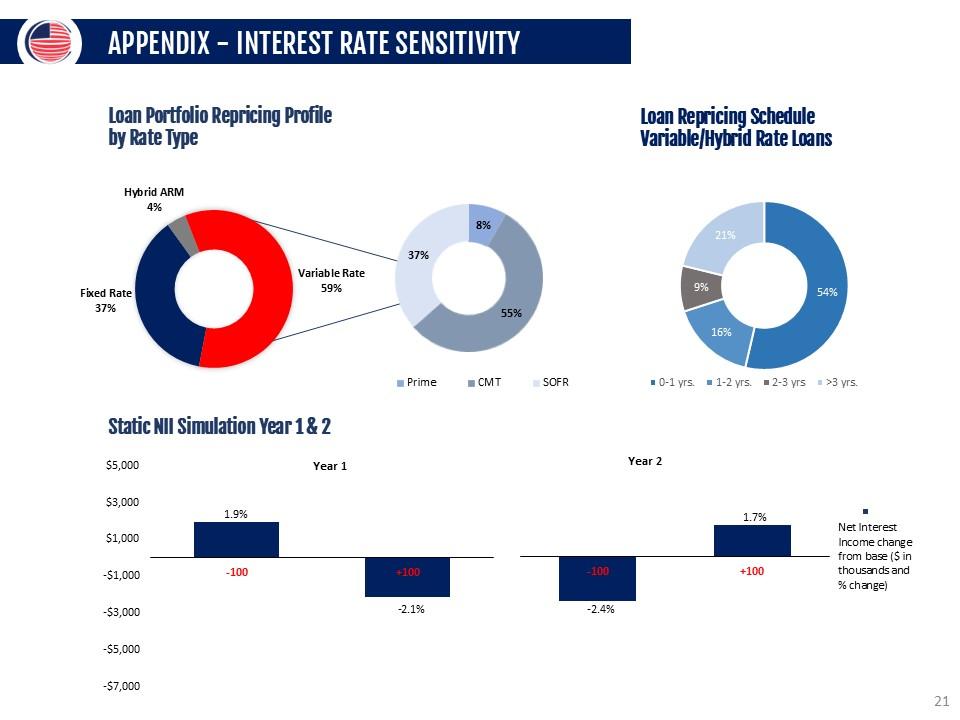

APPENDIX - INTEREST RATE SENSITIVITY Loan Portfolio Repricing Profile by Rate Type Hybrid ARM 4% Fixed Rate 37% Variable Rate 59% 37% 8% 55% Loan Repricing Schedule Variable/Hybrid Rate Loans 21% 54% 16% 9% 0-1yrs. 1-2 yrs 2-3 yrs. 3 yrs. Static NII Simulation Year 1 & 2 Net Interest Income change from base ($ in thousands and % change) Year 1 Year 2 1.9% -2.1% -100 +100 -100 +100 21

CONTACT INFORMATION LOU DE LA AGUILERA Chairman, President & CEO (305) 715-5186 laguilera@uscentury.com ROB ANDERSON EVP, Chief Financial Officer (305) 715-5393 rob.anderson@uscentury.com INVESTOR RELATIONS InvestorRelations@uscentury.com 22